Emergency Savings Should Not Be Treated as a Character Test

Saving money matters, but many households are trying to build a cushion while ordinary life keeps draining the room they need to do it.

Save Article

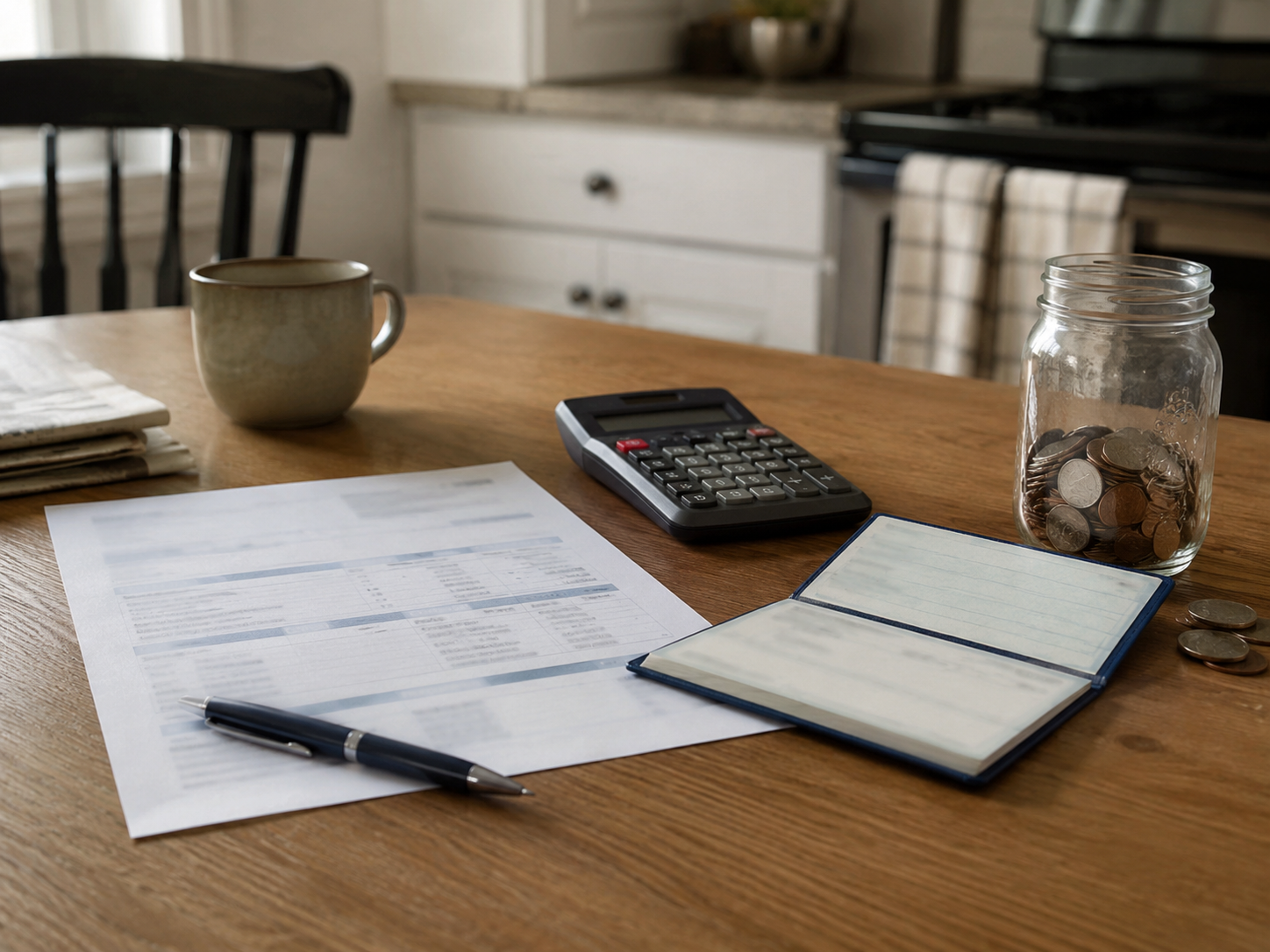

Emergency expenses can expose how little financial room many households have, even when they are trying to manage carefully. Editorial illustration by TheDailyGlobe.

One car repair can change the whole month.

The bill lands on the kitchen table next to a calculator, a checkbook and the small pile of money that was supposed to last until payday. Maybe it is not a car repair. Maybe it is a broken refrigerator, an emergency dental visit, a medical copay, a school expense, a rent increase or a utility bill that arrived higher than expected.

The advice is familiar: everyone should have emergency savings.

That advice is true. It is also incomplete.

Emergency savings matter. They can protect people from high-interest debt, late fees, missed payments and the stress of having no margin. But the lack of savings should not automatically be treated as proof that a person is careless, irresponsible or bad with money.

Ordinary Life Keeps Becoming the Emergency

The Federal Reserve’s 2025 household well-being report covers financial well-being, expenses, credit access, housing, childcare, student loans and economic hardship. The Federal Reserve also reported that price increases remained a common financial concern.

That matters because emergency savings are not built in a vacuum. They are built after rent or mortgage payments, groceries, insurance, childcare, transportation, utilities, student loans, medical costs and debt payments have already taken their turn.

For some households, the problem is not that they do not understand the value of saving. The problem is that the budget has no quiet corner left. A family can work, budget, delay purchases, cook at home, skip extras and still find that one unexpected bill wipes out whatever progress they made.

Financial Advice Can Be Useful Without Becoming Scolding

There is a fair counterpoint here. Savings habits still matter. Budgeting tools can help. Some families do find room by tracking spending, reducing subscriptions, planning meals, refinancing debt or setting up automatic transfers, even if the amount is small.

That should not be dismissed. Personal responsibility is real. People make choices, and some choices help create more stability than others.

But personal responsibility and structural pressure can both be true at the same time. A person can make better choices and still face wages that do not leave enough room, rent that rises faster than income, childcare that consumes a paycheck, medical costs that arrive without warning, or credit terms that make one bad month harder to escape.

The Shame Does Not Help

Pew Research Center reported in 2025 that a majority of adults described their personal finances as only fair or poor. The Federal Reserve said financial well-being declined for young adults, low-income families and Black adults in its 2025 household report summary.

Those findings do not mean every household faces the same pressure, and they do not erase individual decisions. They do show that financial strain is not rare, imaginary or limited to people who failed to follow basic advice.

The public conversation should encourage savings without turning savings into a character test. Shame does not fix a transmission. It does not lower rent, make childcare available, reduce a medical bill or create a better-paying job. It mostly makes people feel alone in a problem that many households are managing quietly.

A Better Test for Financial Resilience

A more honest question is not only whether people are saving enough. It is whether wages, benefits, housing costs, childcare systems, credit access and local prices leave people actual room to save.

That does not turn every financial problem into someone else’s responsibility. It does ask employers, lenders, policymakers and communities to look beyond the slogan. A household cannot build a cushion if every ordinary expense has already become a stress test.

Readers should watch wages, prices, credit access, benefit design, housing costs, childcare costs and local cost pressures. They should also be careful about advice that turns a useful habit into a moral ranking.

The goal should be simple: help more people build real financial breathing room. That requires personal effort, but it also requires systems that do not consume every dollar before savings can begin.

Emergency savings are important. Treating the absence of them as a character flaw is not wisdom. It is a shallow way to talk about a hard problem.

Reporting note: Reporting draws on official household finance data, Federal Reserve materials, Pew Research Center survey reporting, and reviewed background materials used to ground the argument. This article was produced with AI-assisted research and reviewed by an editor before publication.