The Subscription Trap Regulators Are Still Chasing

Recurring charges can quietly drain family budgets, and federal regulators are still focused on subscription signup and cancellation practices.

Save Article

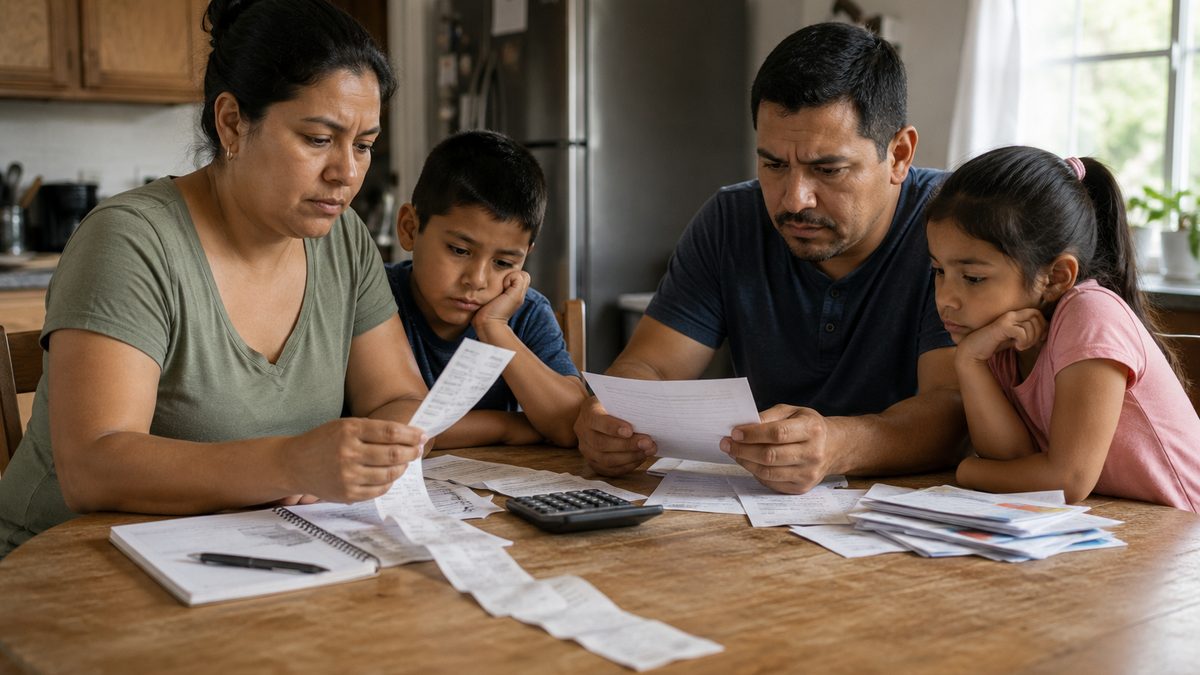

Small recurring subscriptions can become a real monthly budget issue when cancellation is confusing or delayed. Editorial illustration by TheDailyGlobe.

Key Facts

- The FTC alleges Uber charged consumers for Uber One without consent, failed to deliver promised savings and made cancellation difficult despite cancel-anytime promises.

- The allegations against Uber are not final court findings.

- The FTC announced a final click-to-cancel rule in 2024 aimed at recurring subscriptions and memberships.

- Subscription and negative-option practices remain a consumer-protection focus for regulators.

- Available records do not show how many households are affected by hard-to-cancel services.

A family looking over a bank statement may spot the problem one small charge at a time. A delivery membership. A streaming service. An app subscription. A fitness trial. A gaming add-on. None of them looks huge by itself, but together they can take real money out of a monthly budget.

That is the quiet power of recurring charges. They do not always feel like a purchase after the first signup. They become background noise, and background noise can be expensive when groceries, rent, gas, insurance and utilities are already taking more of the paycheck.

Federal regulators are still focused on that problem. The Federal Trade Commission has pursued subscription and cancellation practices through rulemaking and enforcement, including a 2026 case involving Uber One and a broader click-to-cancel rule announced in 2024.

Why Small Monthly Charges Matter

A single subscription may not break a budget. The problem is the stack. Families may carry several recurring charges at once, often spread across phones, laptops, app stores, delivery services, entertainment platforms and free trials that later become paid plans.

For lower-middle-income households, the timing matters. A $9.99 or $14.99 charge can hit the same week as groceries, gas, rent, child care, car insurance or an electric bill. A forgotten charge may not be large enough to trigger a crisis, but it can shrink the cushion families rely on to get through the month.

The issue becomes more frustrating when cancellation is harder than signup. If a service can be joined in a few taps but takes multiple steps, unclear screens, repeated prompts or customer-service hurdles to cancel, the cost can continue after a family thinks it has made a decision to stop paying.

What the FTC Is Alleging Against Uber

The FTC’s case against Uber focuses on the company’s Uber One subscription service. According to the FTC, Uber charged consumers for Uber One without consent, failed to deliver promised savings and made cancellation difficult despite promises that consumers could cancel anytime.

Those are allegations, not final court findings. That distinction matters. The case should not be read as a completed legal conclusion that Uber violated the law. It should be read as part of a broader regulatory focus on how companies enroll consumers in recurring charges and how easily consumers can leave.

The case is useful for readers because it puts a familiar household problem into legal terms. Many consumers do not think about subscriptions as regulatory issues. They think about them as charges they forgot, bills they cannot easily cancel or savings that did not appear the way they expected.

The Broader Click-to-Cancel Push

The FTC announced a final click-to-cancel rule in October 2024, saying it was aimed at making it easier for consumers to end recurring subscriptions and memberships. The agency framed the rule around a basic principle: ending a subscription should not be harder than starting one.

The rule fits into a larger concern about negative-option billing, where a consumer’s silence, inaction or failure to cancel can be treated as permission to keep charging. Recurring billing is not automatically deceptive. Many subscriptions are clear, useful and easy to cancel. The consumer risk comes when the terms are unclear, consent is disputed, savings are overstated or cancellation becomes a maze.

That difference is important. This is not an argument that every subscription service is a trap. It is a warning that the structure of recurring billing can create budget risk when companies make the monthly charge easier to start than to stop.

The Family-Budget Leak

Subscription costs are easy to underestimate because they arrive in pieces. A family may remember the biggest bills but miss the smaller ones. A streaming service renewed on one card, a delivery plan on another, an app charge through a phone account and a trial that converted after a busy week can add up before anyone notices.

For families trying to clean up a budget, recurring charges can be one of the hardest categories to track. They may not come due on the same day. They may use different billing names. Some may be attached to accounts set up by different family members. Others may be tied to services the household still uses, making the decision less obvious.

Small businesses face a related trust issue. Many local companies use recurring billing tools for memberships, services, classes, subscriptions or software. Clear terms and simple cancellation can matter not only for compliance, but also for customer confidence. If consumers feel trapped, trust erodes quickly.

What Remains Unclear

The Uber case remains unresolved based on the information reviewed here. It is not yet clear how the case will end or what it will mean for the company’s subscription practices.

It is also unclear how future subscription rules and enforcement actions will change cancellation practices across the wider market. Regulatory action can push companies to adjust, but the practical effect depends on legal outcomes, compliance, enforcement and how companies design signup and cancellation flows.

Another missing piece is household-level data. Available records do not show exactly how many families are affected by difficult cancellation practices or how much money they lose to unwanted recurring charges. The problem is visible enough for regulators to pursue, but the full family-budget impact is harder to measure.

What Readers Should Watch Next

The next signals will come from FTC enforcement actions, court filings in subscription cases and company changes to cancellation processes. Those updates will show whether regulators are gaining ground and whether businesses are making recurring charges easier for consumers to control.

For families, the larger issue is simple: recurring billing can make small decisions last longer than people intended. A subscription that was useful in January may be forgotten by June. A free trial can become a monthly charge. A cancellation that takes too long can turn into another billing cycle.

That is why subscription practices are not just a tech or legal story. They are a household-budget story. When money is tight, even small charges deserve clear consent, honest promises and an exit door that is easy to find.

Reporting note: Reporting draws on Federal Trade Commission legal filings, FTC rulemaking materials, consumer-protection records, and reviewed household budget context. This article was produced with AI-assisted research and reviewed by an editor before publication.