Emergency Savings Remain Thin as Prices Keep Pressuring Households

Bankrate’s emergency savings data shows why many households still feel financially fragile, even when parts of the economy appear steady.

Save Article

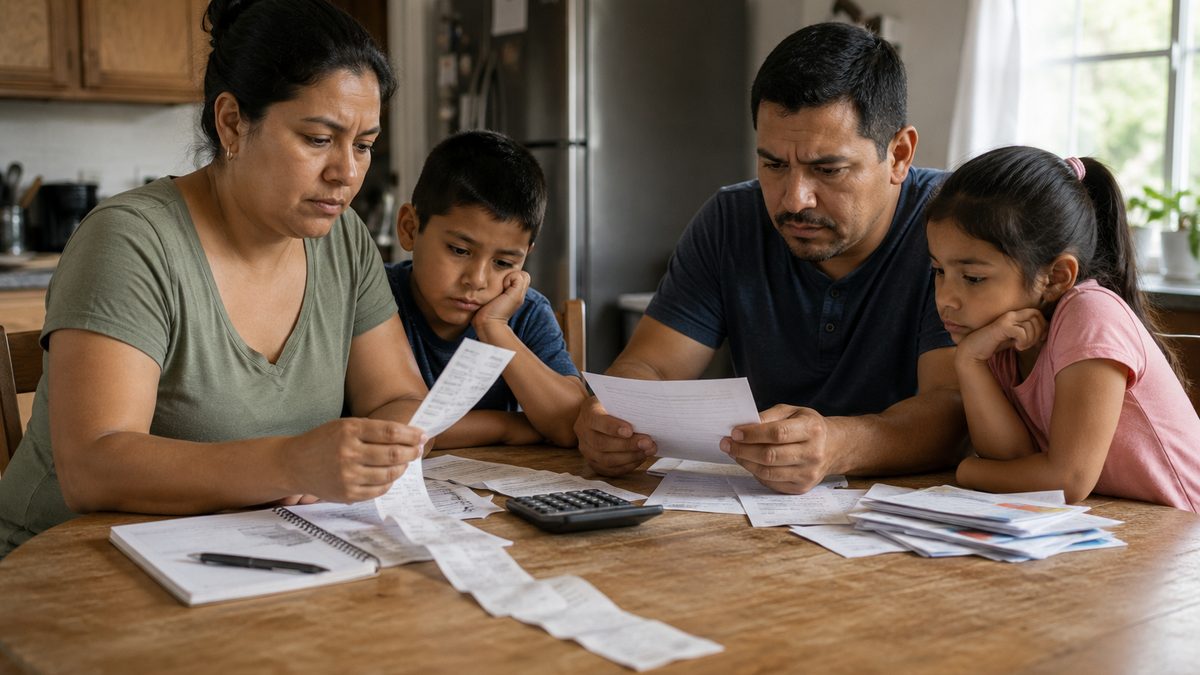

Bankrate’s emergency savings data shows why many households still feel financially fragile, even when parts of the economy appear steady. Editorial illustration by TheDailyGlobe.

Key Facts

- Bankrate’s 2026 emergency savings report found more than half of Americans were uncomfortable with their emergency savings.

- Bankrate reported 58% of U.S. adults said they had less emergency savings or about the same amount as a year earlier.

- Bankrate reported 30% of people would use savings to pay for a major unexpected expense such as a $1,000 emergency.

- The Bureau of Labor Statistics describes the Consumer Price Index as a measure of average price changes paid by urban consumers.

- CBS News maintains a price tracker using BLS data for household cost categories including food, gas, utilities and housing.

Emergency savings remain thin for many households, a sign that everyday financial pressure has not gone away even when some broad economic indicators look stable.

Bankrate’s 2026 emergency savings report found that more than half of Americans were uncomfortable with their emergency savings. The report also found that 58% of U.S. adults said they had less emergency savings or about the same amount as a year earlier.

That matters because emergency savings are one of the clearest measures of household resilience. A family may be employed, paying bills and avoiding crisis, but still be one unexpected car repair, medical bill or missed paycheck away from serious stress.

Why Emergency Savings Matter

Emergency savings are not a perfect measure of financial health, but they tell readers something practical. They show whether households have a cushion when ordinary life becomes expensive in a hurry.

Bankrate reported that 30% of people would use savings to pay for a major unexpected expense such as a $1,000 emergency. That figure shows that some households do have money set aside. It also leaves open a harder question: what happens to everyone else when the same kind of emergency arrives?

For many families, a $1,000 surprise is not a rare event. It can be a dental bill, a broken appliance, a car repair, a home repair, a pet emergency or a medical cost not fully covered by insurance. If savings are thin, those costs can spill into credit cards, payment plans, delayed bills or borrowing from relatives.

Prices Still Shape the Savings Picture

The inflation picture can be confusing because headline numbers often sound calmer than lived experience. The Bureau of Labor Statistics describes the Consumer Price Index as a measure of average price changes paid by urban consumers. That helps track inflation, but it does not mean every household feels the same pressure.

CBS News maintains a price tracker using BLS data for household categories such as food, gas, utilities and housing. Those are the categories that often matter most in daily budgeting because they are regular, visible and hard to avoid.

When prices stay high in essential categories, saving becomes harder. A household may not be falling behind every month, but it may also not be getting ahead. That is where financial pressure can hide: not in one dramatic event, but in the slow loss of room between income and expenses.

The Pressure Is Not the Same for Everyone

The Bankrate survey data gives a useful national picture, but it does not show each household’s full financial condition. Savings levels vary widely by income, age, debt, family size, region and job stability.

A household with stable income and low debt may be able to rebuild savings after a setback. A household already facing high rent, childcare, medical costs or irregular work may have much less room. The same grocery bill, gas fill-up or utility increase can feel very different depending on the rest of the budget.

That is why it is important not to flatten the story into one national mood. Some households are doing fine. Others are employed but stretched. Others are already relying on credit or family support to bridge gaps. Emergency savings data helps explain why people can hear that the economy is stable and still feel exposed in their own lives.

What the Data Can and Cannot Tell Us

The data shows discomfort and limited savings capacity, but it does not explain every cause for every household. A person may have low savings because of inflation, debt, medical costs, job disruption, family obligations, low wages, recent emergencies or a mix of several pressures.

It also does not tell readers what to do with their money. Household finance decisions depend on income, debts, obligations, health, job security and local costs. The useful role of this data is not advice. It is context.

That context is clear: many Americans do not feel financially cushioned. Prices for everyday necessities still shape how much room households have to save. And when savings are thin, even a stable month can feel fragile because one unexpected bill can change the whole picture.

For readers, that helps explain the gap between official economic measures and household anxiety. A family can be working, spending carefully and still feel uncertain. Emergency savings are where that uncertainty often shows up first.

Reporting note: Reporting draws on Bankrate consumer survey data, U.S. Bureau of Labor Statistics inflation materials, CBS News price-tracker context, and reviewed background materials on household financial pressure. This article was produced with AI-assisted research and reviewed by an editor before publication.