A Bank Can Deny You a Checking Account Because of a Report You Have Never Seen

Checking account screening reports can affect whether people are approved for bank accounts, but consumers have rights to review and dispute inaccurate information.

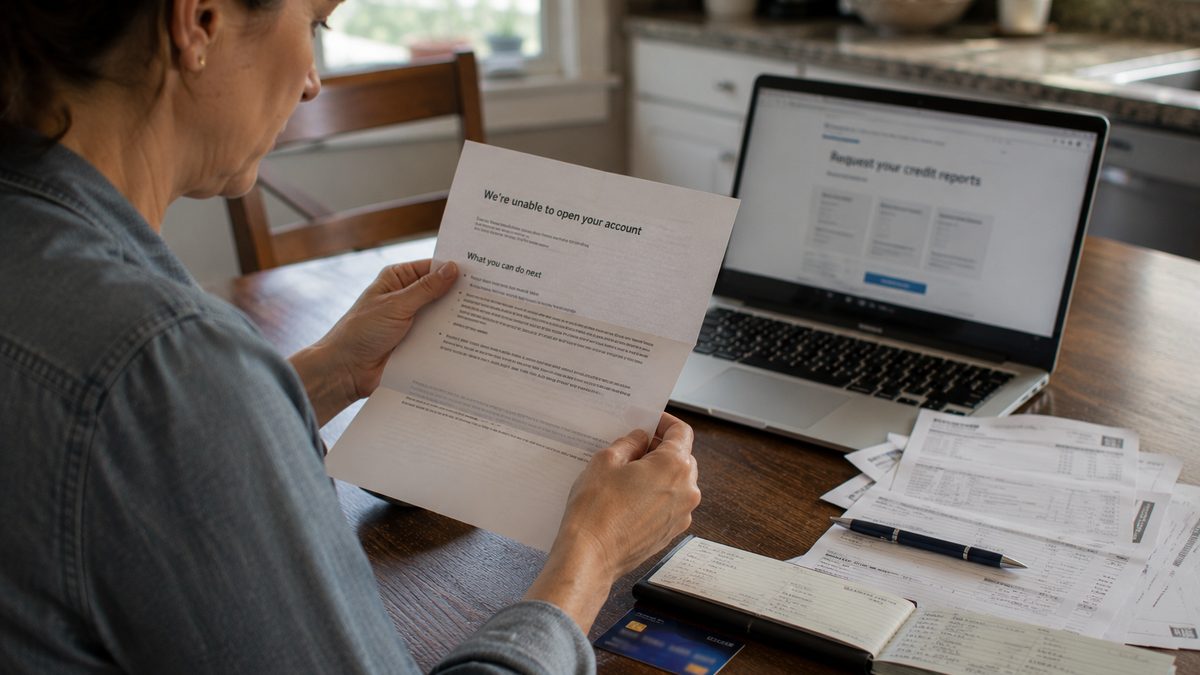

Consumers may have the right to review the checking account report used when a bank denies a new account application. Editorial illustration by TheDailyGlobe.

Key Facts

- Banks and credit unions may use checking account screening reports when deciding whether to approve a new account.

- If an application is denied because of a consumer report, the denial notice should identify the reporting company used.

- Consumers have the right to request a copy of their checking account consumer report and dispute inaccurate information.

- ChexSystems is one of several consumer reporting companies that may collect information about checking account history.

- Some financial institutions offer second-chance or lower-risk checking accounts for applicants who do not qualify for a standard account.

Imagine starting a new job and heading to a bank to open a checking account so your paycheck can be deposited directly. Instead of walking out with a debit card, you are told the application has been denied. You know your credit score is fine, so the decision comes as a surprise. What many people do not realize is that some banks and credit unions use checking account screening reports that are separate from traditional credit reports.

Why Banks Use These Reports

Checking account screening reports are designed to help financial institutions evaluate potential risk when opening new accounts. According to the Consumer Financial Protection Bureau, banks and credit unions establish their own policies for how they use this information. A denial does not automatically mean someone has done anything wrong. It simply means the institution's policies, combined with the information available in the report, did not support approving the application.

Financial institutions may review information related to previous checking account applications, account openings and closures, unpaid negative balances, or check-writing history. Some reports may also contain fraud-related information that banks consider when evaluating new customers.

What Happens After a Denial

If a bank denies a checking account because of information contained in a consumer report, the CFPB says the denial notice should identify the consumer reporting company that supplied the report. That information is important because it tells consumers where they can request a copy of the report used in the decision.

Seeing the report allows consumers to understand what information the bank reviewed. In some cases, the information may be accurate. In others, consumers may discover mistakes or outdated information that should be corrected.

How to Review and Correct a Report

The CFPB says consumers have the right to request a copy of their checking account consumer report from the reporting company. Reviewing the report gives people an opportunity to verify that the information is complete and accurate.

If a consumer believes information is incorrect, federal law provides a process for disputing inaccurate information with the reporting company. Supporting documentation may help resolve errors, although the exact process can vary depending on the company involved.

Alternatives May Be Available

Being denied one checking account does not necessarily mean someone will never qualify for banking services. Some banks and credit unions offer second-chance checking accounts or other products designed for customers rebuilding their banking history. These accounts may include additional restrictions or features intended to reduce overdraft risk while allowing customers to establish or rebuild a positive account history.

Because each financial institution sets its own policies, available options can differ from one bank or credit union to another. Consumers who are denied at one institution may find different products available elsewhere.

What Consumers Should Remember

Checking account screening reports receive far less attention than credit reports, yet they can affect whether someone is approved for a basic checking account. Understanding that these reports exist—and knowing that consumers have the right to request and review them—can make the process less confusing if an application is denied.

A denial is not proof that a report contains errors, nor does it automatically mean someone cannot open an account elsewhere. Reviewing the report, correcting any inaccuracies, and asking about alternative account options are practical next steps that may help consumers move forward while avoiding unnecessary frustration.

Reporting note: Reporting draws on Consumer Financial Protection Bureau guidance covering checking account denials, consumer reporting companies, and consumer rights related to bank accounts. This article was produced with AI-assisted research and reviewed by an editor before publication.